If you get into an accident, you may require medical treatment long before you get money from the person that caused the accident. This treatment is often paid for by your insurance company.

Subrogation is a legal term that simply means that your insurance company can recover the money it paid to you for your injury – but can collect it from the at-fault party that caused your injury. In your personal injury lawsuit, the subrogation payment will come out of the compensatory damages the other party’s insurance company will pay.

It’s as if your insurance company says to you:

“Look, right after your accident, we paid all of your medical bills. Now you got a settlement that is designed to pay, at least in part, compensation for your medical care. That part of the money should go to us.”

Subrogation can apply to payments made by your insurance company to you related to:

To protect your right to the damages from your accident, the subrogation payments to your insurance company are limited by:

In this article, our California personal injury attorneys will answer these faqs about the insurance subrogation process:

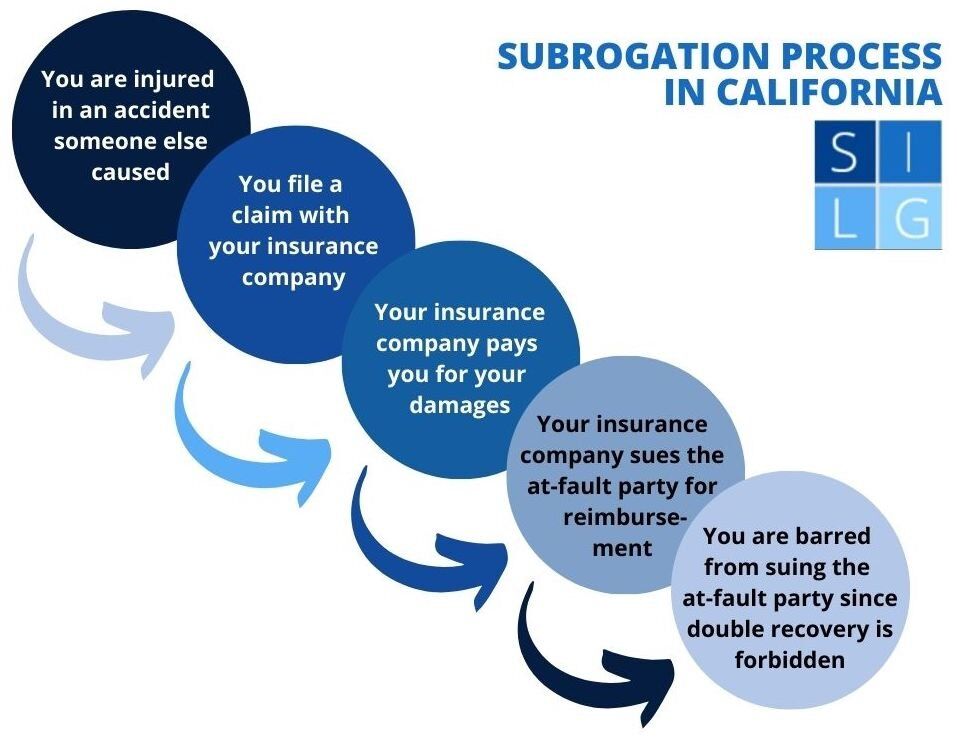

Subrogation is a legal process for the companies that make first payments eventually to be paid back by the person at fault.

In a personal injury claim, you file a lawsuit against the person that harmed you, to get money for your losses.

Oftentimes you will receive payments from your own insurance company or another provider before you recover money from the person at fault. You may receive

Whatever benefits you receive before the end of your lawsuit should be the responsibility of the person who caused the accident. Subrogation is a way for the companies that make these first payments eventually to be paid back by the person at fault.

Subrogation has been described as:

The right of subrogation for an insurance company:

Under California state law, the elements of an insurance company’s cause of action for subrogation are:

Example of subrogation:

Your insurance company has no subrogation rights against you.

Your insurance company has no subrogation rights against you as the policyholder, meaning the insurance company cannot pay money to you and later ask you to pay it back. Subrogation only allows the insurance company to go after someone else.

You bought the insurance to cover your loss. If the insurance company could get the money back from you, the insurance would be worthless.

There is no subrogation right when you are at fault in an accident. You have no one to sue and recover money from because it was your fault. Since the insurance company steps into your shoes, they also have no one to pursue to get their money back. 3

There are three types of subrogation:

An insurance policy will often require your cooperation with the insurance company’s subrogation efforts. You cannot take any action that jeopardizes the insurance company’s right to recover the money it paid you.

For example, you cannot sign an agreement releasing the party at fault in exchange for them paying your insurance deductible. This may help you but will hurt the insurance company’s ability to get their money back. 5

The process of subrogation can apply in any situation where a payment was made to someone other than the primary person responsible. The following situations are common in personal injury claims.

Medical Pay (Med-Pay) is part of an auto insurance policy that allows you to send your medical bills from an accident for payment by your own auto insurance. It gives an added source of money (beyond comprehensive collision coverage) for medical treatment if you are injured.

However, there is no requirement for an insurance company to provide this. It is something that is negotiated between you and your insurance company.

Med-Pay payments that your insurance company wants to be reimbursed for must come from whatever you recover from the party at fault. The insurance company cannot sue the party at fault directly for this. 6

Example: Jill is involved in an auto accident that is the fault of Bob. She receives chiropractic treatment totaling $1,000 and submits this for payment to her insurance company. The insurance company pays this amount per the Med-Pay portion of her auto insurance contract.

Jill then receives a $10,000 settlement from the at-fault driver’s insurance company. Out of this her insurance company is reimbursed for the $1,000 it paid for the chiropractic treatment.

Essentially the insurance company loaned Jill $1,000 for medical treatment until she could collect the money from Bob and pay back the insurance company.

An insurer paying an insurance claim under your uninsured motorist coverage can use subrogation to get reimbursed by the responsible party

An insurance company paying a claim under your uninsured motorist coverage can use subrogation to get reimbursed by the responsible party. A subrogation clause in your insurance contract may state:

“if we (the insurance company) make a payment under the uninsured motor vehicle coverage, we have the right to recover the amount of our payment from any person legally responsible for the loss. You (the policyholder) must transfer all rights to recover to us, execute all legal papers we need, and not harm our rights to recover from the responsible party.”

It is the insurance company’s responsibility to try to obtain money from the uninsured motorist who caused the accident. 7

Example: Joe is involved in a head-on collision accident and the other driver, Sam, is at fault but does not have auto insurance. Joe receives payments for his damages of $25,000 from his insurance company under the uninsured motorist provision of his auto policy. His insurer has subrogation rights to “step into Joe’s shoes” and go after Sam for the amount of the claim paid to Joe. After all, Sam is the person at fault.

Whether the insurance company is successful at getting any money from Sam has no effect on Joe keeping the $25,000. If Sam is uninsured, it’s unlikely he will have $25,000 to pay back the insurance company, and they will never get their money back.

Subrogation does apply in lawsuits for workplace injuries in California. You have a right to file both a workers’ compensation claim and a civil claim if your work injury was caused by someone else while you were working.

Your employer, through its workers’ compensation insurance carrier, can

If either you or the workers’ compensation insurance company files a civil lawsuit against the third party, you are to notify the other.

The workers’ compensation carrier can file a lien in lieu of joining the matter. The lien can be updated up until the time of judgment if the insurance company continues to pay you benefits. See below for a discussion of liens.

The Common Fund Doctrine applies here. 8 See below for a discussion of the Common Fund Doctrine.

Any funds you receive from the person at fault after attorney fees, expenses, and payment of the employer’s lien will relieve the workers’ compensation insurance company of having to make further payments to you until those funds are used up.

Example: Jack drives a delivery truck and is involved in an auto accident that is the fault of Chris. Jack files a workers’ compensation claim and receives medical care and temporary disability benefits totaling $30,000.

Jack files a trucking accident lawsuit against Chris and receives a settlement of $100,000 that factors into his medical treatment and disability.

The workers’ compensation insurance company has a right to recover the $30,000 in payments it made to Jack. If they could not, Jack would get $30,000 in workers’ compensation benefits and the same amount would be counted again in his settlement with Chris, meaning that he would be getting paid double.

Moreover, the worker’s compensation insurance company does not have to make further payments to Jack until he spends up to $70,000 on benefits the insurance company would have given if he didn’t receive money from the person at fault.

See 7.1 Health Insurance and Cal. Civ. Code § 3040 below.

Subrogation often occurs at your expense as it reduces the total amount of money you receive in your pocket.

Subrogation often occurs at your expense as it reduces the total amount of money you receive in your pocket. There are protections in place to prevent entire settlements from being used up reimbursing insurance companies who initially made payments before the party at fault pays for it.

Cal. Civ. Code § 3040 deals with the reduction of health insurance bills in personal injury cases. Section 3040 places a limit on what an insurance company can recover out of a settlement for payments made to you.

(There is often contractual language in your healthcare insurance contract that may allow them to go outside of the Made Whole Doctrine. See below for a discussion of the Made Whole Doctrine.)

The insurance company is limited in its recovery by the lesser of:

The cost of the medical services depends on how the insurance company pays medical providers. This is based on a concept called capitation.

Capitation is a set fee paid by an insurance company to a doctor for each person it treats regardless of the services provided. Alternatively, in a non-capitated setting, the health insurance company pays doctors based on the actual medical services provided.

Some health insurance plans pay medical providers

In a non-capitated case, it is easy to figure out what medical care you had that was related to the accident because you can just look at the charges to determine the first factor.

Though in a case where the insurance company pays a set fee for each person a doctor treats, how do you figure out what part of those payments was for medical treatment related to the accident?

Section 3040 says that those paid on a capitated basis are limited to 80% of the usual charge by medical providers on a non-capitated basis. In this way, they can get a reasonable estimate of the cost of the treatment for the first factor.

Once you figure out the cost of the medical services – the first factor – you must look at the second factor so that you can take the lower value of the two factors, as required by the statute.

The second factor depends on whether you retained a car accident attorney. If you did have an attorney, the second factor is one-third of the settlement amount. If you did not have an attorney, the second factor is one-half of the settlement amount. 9

Example: Jane had $15,000 in medical bills and received an $18,000 settlement. The medical services costs on a non-capitated basis are $12,000. Jane did not have an attorney, so based on the total settlement, the insurance company could collect one half of the settlement, or $9,000. As this is less than the $12,000 in medical costs, this is the most the insurance company could collect from the $18,000 settlement.

If Jane did have an attorney, the insurance company could collect only one-third, or $6,000, out of the settlement.

The Common Fund Doctrine also applies here.

You and your insurance company are going after the same pool of money from the person at fault.

The Made Whole Doctrine says that a settlement must make you whole before reimbursing the insurance company. This may come up if the person at fault does not have enough insurance to cover your loss. 10

Example: Jane is involved in a motorcycle accident that is the fault of Justin. Her auto insurance company under a Med-Pay plan pays $1,000 for Jane’s chiropractic treatment. Jane has damages totaling $18,000 but only receives a $15,000 settlement from Justin.

Jane has not been made whole because her damages of $18,000 are more than her settlement of $15,000. Therefore, she can use the Made Whole Doctrine to argue that her insurance company should not be reimbursed for the $1,000 in chiropractic treatment it paid for. If they were, it would be taken out of Jane’s $18,000.

Note that the Made Whole Doctrine may not actually make you whole because your car accident attorney obtains his or her fee from your settlement.

Example: Jane’s personal injury attorney will take a one-third fee out of her $18,000 settlement. She will only pocket $12,000. For Jane to be made whole, the settlement would have to be $24,000. This would give her the damages she suffered of $18,000 and pay an attorney fee of $6,000. Jane cannot claim that the made whole calculation should factor in the attorney fee.

You should be aware that the Made Whole Doctrine may be overruled by language in the insurance contract that gives the insurance company “all rights of recovery to the extent of its payment.”

The Common Fund Doctrine makes insurance companies pay part of the money it recovers to your attorney if the insurance company does not have its own attorney.

The Common Fund Doctrine makes insurance companies pay part of the money it recovers to your attorney if the insurance company does not have its own attorney.

Since your attorney put in the effort to resolve the case – including getting the insurance company their money back – the attorney should receive a fee out of the insurance company’s recovery for their effort.

This gives your attorney an incentive to handle the insurance company’s subrogation claim. Even though the insurance company did not hire its own attorney, it should still pay some of the cost of getting its money back. 11

Example: Nancy is involved in an auto accident where Mark was at fault. Her car insurance company pays $6,000 in medical expenses. Her lawsuit against Mark results in a settlement of $24,000. The insurance company did not take part in the legal action. Without the Common Fund Doctrine, the insurance company could receive $6,000, but why should it get all of its money when it didn’t even hire its own attorney?

With the Common Fund Doctrine, the attorney’s fee of one-third, or $8,000, is paid in part out of the insurance company’s recovery.

The insurance company will only receive $4,000. This is the $6,000 they paid for medical treatment minus a one-fourth share of the $8,000 attorney fee. The one-fourth comes from the fact that $6,000 is one-fourth of the $24,000 settlement.

For Nancy, without the Common Fund Doctrine, she would get $10,000, which is $24,000 less the $8,000 attorney fee and the $6,000 to the insurance company. But with the Common Fund Doctrine, the deduction is $8,000 for the attorney fee but only $4,000 for the insurance company, and Nancy will pocket $12,000.

The following terms refer to a payment by someone who was not primarily responsible for the payment. In these cases, though, they are not standing in your shoes, even though the result is a similar recovery of money.

Contribution is often confused with subrogation. However, it does not place a person in the shoes of another. It is a separate right.

This may occur when

Each insurance company has the right to seek contribution from the other if it paid more than its fair share because both insurance companies are primarily liable for the loss. This does not affect your rights.

However, even if two insurance companies cover you, there may be a subrogation right if one insurance company is not primarily liable for the loss. 12

Example: Alpha Insurance and Beta Insurance both insure Maria equally for the same accident. If Alpha pays Maria’s entire damages of $20,000, Alpha can pursue a contribution claim against Beta for 50% of the amount they paid. In this case, that would be $10,000. This has nothing to do with Maria’s rights.

Reimbursement is a right to receive a payment back for what has been paid by the insurance company. It is not a legal right to step into your shoes, but it does give the insurance company the right to recover payments out of the settlement.

Subrogation and reimbursement are often used interchangeably. In California, the subrogation and reimbursement right of an insurance company are often referred to as subrogation rights. 13

A lien is an independent right of an insurance company to recover money from a settlement. The settlement will not be distributed to you until the lien is paid.

A lien can be created

For more in-depth information, refer to these scholarly articles: